How to avoid falling back into debt

Avoid Falling Back Into Debt Habit Budget Tip Mind: Your Complete 2025 Guide to Financial Freedom

Learning how to avoid falling back into debt habit budget tip mind is one of the most critical financial skills you can develop in today’s economy. After working hard to pay off debt, the last thing you want is to find yourself back at square one, drowning in financial obligations and struggling with minimum payments. This comprehensive guide will equip you with proven strategies, practical tools, and actionable steps to ensure your debt-free status remains permanent. Whether you’re fresh off paying down significant debt or preparing yourself for the challenges ahead, understanding the psychology and mechanics of debt prevention is essential. We’ll explore everything from building sustainable habits to identifying warning signs before they become problems, all designed to help you maintain your hard-earned financial independence.

Table of Contents

- Why Avoid Falling Back Into Debt Habit Budget Tip Mind Matters

- Step-By-Step Avoid Falling Back Into Debt Habit Budget Tip Mind Guide

- Best Avoid Falling Back Into Debt Habit Budget Tip Mind Options

- Pro Tips for Avoid Falling Back Into Debt Habit Budget Tip Mind

- Common Mistakes to Avoid

- Key Takeaways

- Frequently Asked Questions About Avoid Falling Back Into Debt Habit Budget Tip Mind

- Conclusion

Why Avoid Falling Back Into Debt Habit Budget Tip Mind Matters

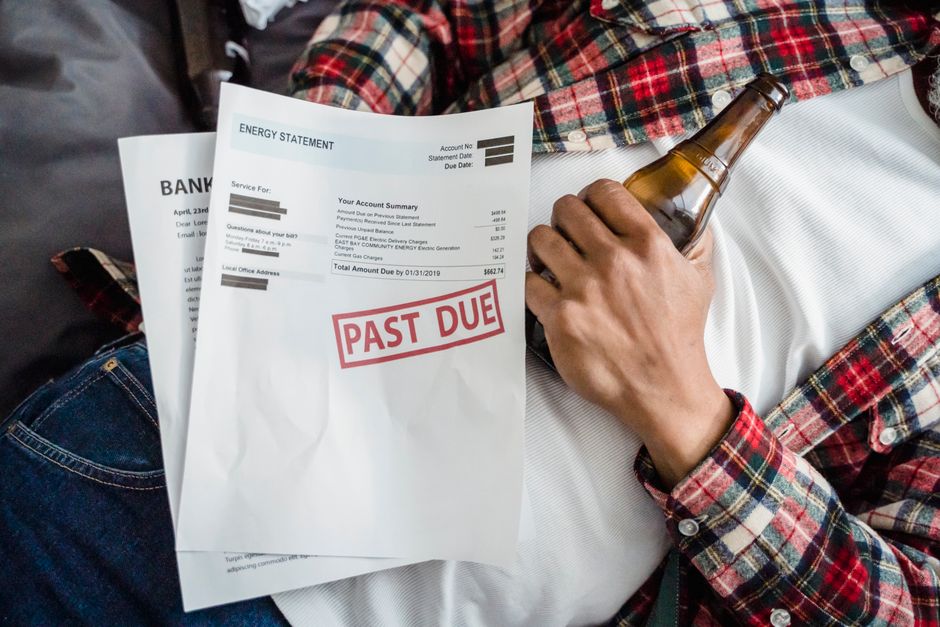

The statistics surrounding debt relapse are staggering and should serve as a wake-up call to anyone who has recently become debt-free. Studies show that approximately 40% of people who pay off debt end up accumulating it again within a few years, often reaching similar or even higher levels than before. This cycle isn’t a sign of personal failure; rather, it reflects how easy it is to slip back into old spending patterns and financial behaviors without a concrete plan to avoid falling back into debt habit budget tip mind.

When you understand why debt relapse happens, you’re better equipped to prevent it. Most people focus exclusively on the mathematical aspect of debt payoff—paying down the principal and interest—but neglect the behavioral and psychological components that led to debt accumulation in the first place. Without addressing these root causes, you’re essentially treating the symptom rather than the disease, leaving yourself vulnerable to repeat the same mistakes.

The emotional relief that comes from becoming debt-free can be dangerous if not properly managed. Many people celebrate their achievement by loosening their financial constraints, thinking they’ve “earned” the right to spend freely again. However, this mindset is precisely what created the debt problem initially and is the fastest path to accumulating new debt within months or years.

Additionally, avoid falling back into debt habit budget tip mind becomes crucial when life throws unexpected challenges your way. Medical emergencies, job loss, or family crises can derail even the most committed debt-free individuals who haven’t built adequate emergency reserves and financial buffers. Without these safeguards in place, you might be forced to return to credit cards and loans, instantly reversing your progress.

The long-term benefits of successfully avoiding debt relapse extend far beyond your bank account. Financial stability reduces stress, improves your mental health, strengthens relationships, and allows you to build wealth through investments and savings rather than payments to creditors. The sense of control and freedom you experience is invaluable and worth protecting with intentional, deliberate strategies.

Step-By-Step Avoid Falling Back Into Debt Habit Budget Tip Mind Guide

Step 1: Perform a Comprehensive Debt Exit Analysis

Before implementing prevention strategies, you need to understand exactly how you accumulated debt in the first place. Sit down and honestly assess your spending patterns, emotional triggers, and decision-making habits that led to borrowing. Were you spending beyond your means trying to maintain a lifestyle? Did you lack a budget? Were there unexpected expenses you couldn’t cover? Understanding these patterns is fundamental to avoiding them in the future.

Document your triggers—the specific situations, emotions, or circumstances that prompted spending you couldn’t afford. Common triggers include stress, boredom, social pressure, emotional eating, or “just one small purchase” that snowballed into multiple debts. Write these down specifically so you can create concrete strategies to address each one.

Step 2: Create a Sustainable Monthly Budget

A budget is absolutely non-negotiable for anyone serious about avoiding falling back into debt habit budget tip mind. However, this isn’t the restrictive, depressing budget many people imagine; instead, it’s a realistic plan that accounts for both necessities and wants while maintaining a debt-free trajectory. Use the 50/30/20 rule as a starting point: allocate 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt prevention.

Make sure your budget is flexible enough to maintain long-term. Overly restrictive budgets typically fail because they feel punitive and unsustainable. Build in reasonable amounts for entertainment, dining out, and hobbies—the activities that make life enjoyable—while ensuring you never spend beyond your means.

Step 3: Establish a Zero-Based Financial System

Every dollar in your budget should be allocated to a specific purpose before you spend it—this is called zero-based budgeting. This system prevents the dangerous scenario where “unallocated” money mysteriously disappears into unnecessary purchases. When you know exactly where every dollar is going, you maintain control and make intentional rather than impulsive financial decisions.

Implement this system by categorizing your expenses before the month begins and tracking your spending against these categories. Many apps make this process simple and automated, removing the friction from responsible financial management. The key is being honest about your allocations and adjusting them if you find certain categories consistently exceed your plan.

Step 4: Build a Robust Emergency Fund

An emergency fund is your primary defense against being forced back into debt when unexpected expenses arise. Most financial experts recommend maintaining three to six months of essential living expenses in a separate savings account, though starting with one month’s worth is completely acceptable if you’re just beginning. This fund prevents the domino effect where one emergency forces you to use credit cards, which then requires more borrowing to cover new expenses.

Start small if necessary—even $500 to $1,000 provides meaningful protection against minor emergencies like car repairs or medical copays. Once you’ve established this starter fund, gradually build toward your three to six-month goal. This process typically takes years, but every dollar added increases your financial stability and your ability to avoid falling back into debt habit budget tip mind.

Step 5: Automate Your Financial Commitments

Automation removes decision-making from the equation and ensures you maintain your debt prevention plan even during busy periods or moments of weakness. Set up automatic transfers to your emergency fund immediately after receiving your paycheck, before you have the opportunity to spend that money. Similarly, automate your bill payments to ensure you never miss a payment and damage your credit recovery.

Automation also works for your savings goals and investment contributions if you’re ready for that step. By making your financial commitments automatic, you align your daily experience with your financial intentions, making responsible behavior the path of least resistance rather than something requiring constant willpower.

Best Avoid Falling Back Into Debt Habit Budget Tip Mind Options

Option 1: The Envelope System (Digital or Physical)

The envelope system is a time-tested method that makes spending tangible and limits you to actual available funds. In the traditional approach, you allocate cash to physical envelopes labeled for different spending categories and can only spend what’s in each envelope. When the envelope is empty, that’s the spending limit for that category until the next budget period.

The digital version works the same way but through budgeting apps that simulate envelopes. This method is particularly effective for people who struggle with overspending because it provides a hard stop—you literally cannot spend money you haven’t allocated. Many people find this approach so effective that they continue using it even after establishing good financial habits.

Option 2: The Debt-Free Mindset Accountability Partnership

Finding an accountability partner—someone else committed to financial health—can dramatically increase your success rate in avoiding falling back into debt habit budget tip mind. This person serves as your financial confidant, someone you check in with monthly about your budget, spending, and financial goals. They provide encouragement during difficult months and gently challenge you when you’re considering purchases that contradict your goals.

Accountability partnerships work because they leverage social pressure positively—rather than feeling ashamed of financial struggles, you have someone who understands and supports your journey. Many successful debt avoiders participate in online communities or local groups where members share their financial progress and challenges, creating a culture of mutual support and shared responsibility.

Option 3: Wealth-Building Financial Planning

Once you’re confident in your ability to stay debt-free, shift your focus toward building wealth through investing and saving. This positive goal orientation is more motivating than the negative framing of “avoiding debt.” By focusing on your investment returns, retirement growth, and wealth accumulation, you create compelling reasons to maintain disciplined spending.

Work with a financial advisor to develop an investment strategy appropriate for your goals and risk tolerance. Contributing regularly to retirement accounts, taxable investment accounts, and educational savings plans provides tangible progress you can track and celebrate. This forward-looking approach keeps you engaged with your financial plan and makes the lifestyle changes necessary to avoid falling back into debt feel worthwhile.

Pro Tips for Avoid Falling Back Into Debt Habit Budget Tip Mind

Implement the 24-Hour Rule for Non-Essential Purchases

Before buying anything that isn’t a budgeted necessity, wait 24 hours. This simple delay eliminates impulse purchases while honoring legitimate wants. Many times, you’ll realize you didn’t actually want the item or you can find a better option at a lower price. This practice conditions your brain to slow down spending decisions and evaluate purchases against your financial priorities.

Remove Temptation from Your Immediate Environment

Unsubscribe from marketing emails, delete shopping apps from your phone, and avoid browsing websites that trigger spending impulses. If online shopping is your weakness, avoid the websites during vulnerable moments—this isn’t about willpower but about designing your environment to support your goals. Psychological research consistently shows that removing temptation is more effective than relying on self-control.

Track Your Net Worth Monthly

Calculate your net worth—assets minus liabilities—at least monthly, though quarterly or annually also works well. Watching this number grow provides powerful motivation and makes your financial progress visible. This metric encompasses your entire financial picture rather than just your income or spending, creating a comprehensive view of your financial health.

Check price on Amazon

Practice Gratitude for Your Debt Freedom

Deliberately reflect on how far you’ve come and acknowledge the effort required to achieve debt freedom. When you feel tempted to spend recklessly, remember the stress and burden of debt and how good it feels to be free from that. This emotional connection to your financial goals makes protecting them feel important rather than like deprivation.

Celebrate Milestones Without Spending

Create meaningful ways to celebrate your financial achievements that don’t involve purchases or experiences requiring debt. Throw a small gathering at home, spend time with loved ones, enjoy free activities, or create a visual representation of your progress. These celebrations reinforce that you’ve accomplished something genuinely meaningful and provide emotional satisfaction without financial setback.

Common Mistakes to Avoid

Mistake 1: Failing to Address the Root Causes of Debt

Many people focus exclusively on paying off debt without examining the behaviors and attitudes that created it. Once the debt is gone, they revert to old patterns because nothing fundamentally changed in their approach to money and spending. To truly avoid falling back into debt, you must identify whether your issue was living beyond your means, lacking financial knowledge, experiencing unexpected expenses, or emotional spending, then directly address that specific cause.

Mistake 2: Becoming Overconfident Too Quickly

The relief and confidence that comes from becoming debt-free can lead to premature relaxation of financial discipline. You might think, “I’ve proven I can manage money—now I can loosen up,” only to find yourself back in debt within a year. Financial success requires maintaining consistent practices indefinitely, not just until you’ve achieved a specific goal.

Mistake 3: Neglecting to Build an Emergency Fund Simultaneously

Many debt-free individuals don’t prioritize emergency savings, assuming they’ll never need to borrow again. When life’s inevitable surprises occur, they’re forced to choose between going without or going back into debt. The emergency fund is as crucial to debt prevention as the debt payoff itself.

Mistake 4: Lifestyle Inflation After Becoming Debt-Free

Once your debt payments stop, you have more available income each month. Rather than directing this toward emergency funds and savings, many people spend it on an upgraded lifestyle—nicer car, bigger home, expensive hobbies. Before you know it, this new spending level exceeds your income just as before. Commit to maintaining your debt-era lifestyle for at least a year after becoming debt-free, allowing you to redirect that money toward financial security.

Mistake 5: Failing to Adjust Your Identity and Self-Image

How you see yourself profoundly influences your behavior. If you’ve internalized an identity as a “spender” or “bad with money,” you’ll unconsciously recreate scenarios that confirm this identity. Consciously work to develop a new identity—”someone who makes intentional financial decisions” or “a wealth builder”—and make choices that reinforce this new self-image.

Key Takeaways

- Root cause analysis is essential: Understand precisely how you accumulated debt so you can prevent history from repeating itself

- Budgeting and automation form your foundation: These systems remove willpower from the equation and make responsible behavior automatic

- An emergency fund is non-negotiable: Three to six months of expenses prevents unexpected situations from forcing you back into debt

- Community support significantly improves success: Accountability partners and financial groups increase your likelihood of maintaining debt freedom long-term

- Wealth-building creates positive motivation: Focusing on what you’re building rather than what you’re avoiding maintains long-term engagement with your financial plan

Frequently Asked Questions About Avoid Falling Back Into Debt Habit Budget Tip Mind

Q: What is the best avoid falling back into debt habit budget tip mind strategy for someone who just paid off all their debt?

A: The most effective approach combines multiple strategies: immediately establish an emergency fund, create and automate a sustainable budget, address the behavioral patterns that created debt originally, and find an accountability partner or community. Start with these foundations before implementing additional wealth-building strategies. Most importantly, maintain your debt-era lifestyle for at least six to twelve months while you stabilize your new debt-free status before making major spending increases.

Q: How do I use avoid falling back into debt habit budget tip mind principles if I have variable income?

A: Variable income requires a slightly different approach: base your budget on your lowest monthly income from the past year, treating any income above that amount as extra to direct toward emergency savings and debt prevention. Use a zero-based budgeting system that adapts monthly as your income varies. Consider taking on a small side income source to stabilize your base income if possible, providing more predictability for your budget planning.

Q: How long does it typically take before avoiding falling back into debt habit budget tip mind becomes automatic?

A: Building new financial habits typically requires 66 to 254 days of consistent practice, with the average being around 66 days. However, truly embedding these habits into your identity and automatic behavior usually takes 6 to 12 months. Be patient with yourself during this period—occasional lapses are normal, and the goal is consistency over perfection, not perfection immediately.

Q: What should I do if I slip up and spend more than budgeted?

A: First, don’t use a single overspending incident as justification to abandon your entire plan—one mistake doesn’t erase your progress. Analyze what triggered the overspending and adjust either your budget (if the category was unrealistically low) or your strategies (if you need better systems to prevent that trigger). Record the lesson and move forward, refining your approach as you learn more about yourself.

Q: How do I handle pressure from friends and family to spend money I’ve budgeted elsewhere?

A: Clearly communicate your financial goals and boundaries to people close to you, explaining that avoiding falling back into debt habit budget tip mind is a priority. You don’t need to be defensive or share detailed financial information—simply say, “That doesn’t fit my budget right now” or “I’m focusing on financial goals this year.” True friends will respect your priorities, and you might inspire others to get their own finances in order.

Conclusion

Learning how to avoid falling back into debt habit budget tip mind is the ultimate test of your financial commitment—anyone can pay off debt with enough focus and sacrifice, but staying debt-free requires building sustainable systems and habits that support your goals indefinitely. The strategies outlined in this guide—from emergency fund building to accountability partnerships to wealth-focused planning—provide comprehensive protection against the debt relapse that affects nearly half of people who achieve debt freedom.

Remember that avoid falling back into debt habit budget tip mind isn’t about deprivation or punishment; it’s about designing a life where your spending aligns with your values and goals. Start implementing these strategies today, be patient with yourself as you establish new habits, and celebrate the progress you make along the way. Your financial independence is too valuable to leave to chance—take control of it through intentional, deliberate action.

Recommended Products on Amazon

As an Amazon Associate I earn from qualifying purchases.